The foreign policy of the European Union (EU) has experienced substantial changes over the last few years. In 2021, the EU announced the launch of the Global Gateway, a new European strategy to boost smart, clean and secure links in digital, energy and transport sectors and to strengthen health, education and research systems across the world. Between 2021 and 2027, the EU will mobilize up to €300 billion of investments. The Union expects that implementation of the program will allow the EU’s partners to develop their societies and economies, and create opportunities for the EU member states’ private sector to invest and remain competitive (European Commission, 2023a). The EU approved 40 investment programs in Sub-Saharan Africa, Latin America, and the Asia-Pacific. It is worth noting that the Union’s participation in the construction of a €5 billion hydropower plant in Tajikistan is of great interest to Central Asia. Many experts remain skeptical about the Global Gateway calling it ‘old wine in new bottles’ or ‘cosmetics to make the European Union feel better’ (Barbero, 2023). However, the Strategy may serve as a good starting point to increase the EU’s global competitiveness and gain geopolitical importance.

The war in Ukraine led to substantial changes in the European Union’s foreign policy and caused a start of a new era. The Union imposed tough sanctions on the Russian economy, including the sensitive energy sector. Moreover, it provides Ukraine financial, military and humanitarian aid. At the same time, the EU’s politicians reconsidered the Union’s role in global politics, which was defined as ‘the birth of a geopolitical Europe’ (Lehne, 2022). Reconsideration of foreign policy priorities will affect all partners of the EU, in particular relations with China which deteriorated before the current geopolitical crisis.

In December 2020, the EU and China concluded the negotiations for a Comprehensive Agreement on Investment. China’s fast-growing market of 1.4 billion consumers, which is far less open to foreign investment than the EU’s, is of great interest to European companies. The agreement contains commitments on market access and regulates issues on state-owned enterprises, subsidies, and forced technology transfers. It also contains China’s commitments to ratifying the International Labor Organization’s fundamental Conventions on the abolition of forced labor (European Commission, 2023b).

However, in May 2021, the European Parliament voted to suspend ratification of the agreement due to political tensions caused by bilateral sanctions following China’s Xinjiang policy. Despite China’s efforts, reviving the deal seems unlikely as European politicians express concern over its implementation (McElwee, 2023).

Multinational corporations play a key role in bilateral relations between the EU and China. However, the rise of China’s local brands affects their market positions. For instance, China’s homegrown companies such as Chery and BYD expand rapidly, making sales of Volkswagen and General Motors shrink. Nevertheless, premium carmakers such as BMW and Mercedes-Benz experience robust growth in China’s market. Therefore, western corporations follow three paths, in particular to divestment, decoupling, or improvement of their competitiveness through substantial investments. German companies follow the third option. For instance, Siemens shifts a significant share of research and development to China, while Volkswagen invests €2.4 billion to establish an autonomous-driving joint venture with the Chinese firm Horizon Robotics (Economist, 2022).

Despite growing tensions and the EU calls for the reduction of single-country dependence, European companies increased their investments in China. It is worth noting that these investments did not come from new firms. Between January and June 2022, the EU FDI in China amounted to €5.5 billion increasing by 15% compared to the same period last year. Estimates show that ‘the top 10 European investors in China in each of the past four years made up nearly 80%, on average, of total European direct investment in the country.’ Despite Berlin considering various measures to reduce the country’s dependence on Beijing, Germany remains a key investor in China. A share of German firms has been 43% of the total over the past four years. Four German companies (Volkswagen, BMW, Mercedes-Benz Group and BASF) contributed 34% of all European FDI into China by value from 2018 to 2021 (Dominguez, 2022). In 2022, the EU’s investments in China surged by a record 92.2% compared to the last year, while investments from Germany increased by almost 53%. Despite calls for a reduction of dependence, especially in Germany, the country’s Chancellor Olaf Scholz visited China in early November to restore communication between the two powers (Huld, 2023).

Why does Germany’s policy towards China remain positive? Figure 1 shows bilateral trade flows between the EU and China, while Figure 2 demonstrates China’s top trading partners from the EU. Data shows that the EU’s exports to China increased from $31 billion in 2002 to $259 billion in 2021. For the same period, the Union’s imports from China surged from $73 billion to $606 billion. Thus, China has a substantial trade surplus with the EU.

Figure 1. The EU’s exports to and imports from China, billion $

Source: The Author’s compilation based on the International Trade Centre (2023) data.

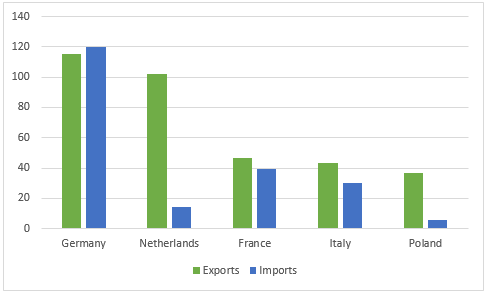

Figure 2. China’s exports to and imports from individual EU countries, 2021, billion $

Source: The Author’s compilation based on the International Trade Centre (2023) data.

For instance, in 2021 China’s exports to the Netherlands amounted to $102 billion, while its imports equaled a low $14 billion. However, the situation with Germany remains different as the country’s exports to China exceed its imports. This is one of the key reasons why German companies continue investing and promoting deals with China.

Despite these bilateral links, there is evidence that the EU’s business in China started its diversification. One of the diversification directions is the Association of Southeast Asian Nations (ASEAN) bloc. In 2021, the EU’s investments in ASEAN equaled $26.5 billion, while in 2020 and 2019 the indicator correspondingly amounted to $18.5 billion and $6.1 billion. Moreover, within the EU’s Global Gateway strategy, European politicians pledged to invest €10 billion into the region. European companies such as LEGO Group and Harvest Waste started their business in the ASEAN (Hutt, 2023). One of the factors of relocation of the EU companies is increasing labor costs in China. Estimates show that between 2013 and 2022 manufacturing wages in China doubled, to an average of $8.27 per hour, which is 3-4 times higher than in other Asian countries, especially members of the ASEAN. For instance, the number of Japanese companies operating in China decreased to 12.700 in 2022 from 13.600 in 2020. Sino-American techno-decoupling also affected the decisions of corporations to relocate their business from China to other countries in Asia (Economist, 2023).

China, in turn, considers its relationship with the EU as a part of its geopolitical rivalry with the United States and pursues three goals towards the Union. In particular, Beijing wants to limit the EU’s support of the US initiatives to contain China. At the same time, China tries to retain its access to EU technologies and market, while it penetrates markets of the Global South. China’s ambassador to the EU Fu Cong proposed to continue work on the EU-China Investment Agreement by eliminating mutual sanctions and dropping the question of the war in Ukraine from the bilateral agenda. Experts label China’s policy towards the EU as a ‘strategic stalling’ calling Brussels to set a new agenda with strategic clarity and embrace more proactive goals beyond risk mitigation (Stec, 2023).

The EU states announce the need to reduce dependency on Chinese investments. China’s FDI in EU-27 and the United Kingdom increased from €7.9 billion in 2020 to €10.6 billion in 2021. This amount of investment was the second lowest year (above only 2020) for China’s investment in Europe since 2013. China mainly invests in the Netherlands, Germany, and France. It is important to note that in 2021, Chinese venture capital investment in Europe more than doubled to a record level of €1.2 billion (Mercator Institute for China Studies, 2022). A ruling coalition in Germany allowed China’s state-owned shipping giant COSCO to buy a stake below 25% in the Port of Hamburg. Initially, COSCO planned to acquire a 35% stake in the Tellerort container terminal. German officials explained it by the existence of a threat to public order and safety. To check national security risks, the EU introduced screening mechanisms, which slowed Chinese FDI. It is worth noting that 40% out of 650 Chinese investments in Europe between 2010 and 2020 had high or moderate involvement by state-owned or state-controlled companies (Harper, 2022).

Thus, the EU policies on China’s policies towards Xinjiang and Hong Kong and other human rights-related issues deteriorated bilateral relations. The EU also criticizes China’s positions on the war in Ukraine. Despite the existence of these contradictions, economic ties between Brussels and Beijing have been strong. It is important to note that while the EU politicians are concerned about human rights, European companies are less interested in such issues continuing their businesses in China. This makes the EU policy towards China complicated as the private sector ignores the policy of the EU. It is worth noting that there is also no united Europe, as members of the EU have different relationships with China at the individual level. However, some EU companies started relocation processes and organized their business in the ASEAN.

Hence, to meet a rival like China, the EU needs to improve its competitiveness, align its political and private sector goals, and adjust its global initiatives and strategies to make them more attractive.

References

Barbero, Michele (2023). Europe is Trying (and Failing) to Beat China at the Development Game. Retrieved from https://foreignpolicy.com/2023/01/10/europe-china-eu-global-gateway-bri-economic-development/. Accessed on 01.03.2023.

Dominguez, Gabriel (2022). Even as China loses its luster, European companies continue to invest. Retrieved from https://www.japantimes.co.jp/news/2022/09/15/business/china-europe-investment/. Accessed on 10.03.2023.

Economist (2022). Multinational firms are finding it hard to let go of China. Retrieved from https://www.economist.com/business/2022/11/24/multinational-firms-are-finding-it-hard-to-let-go-of-china. Accessed on 14.03.2023.

Economist (2023). The growing alternatives to ‘made in China’. Retrieved from https://www.afr.com/world/asia/the-growing-alternatives-to-made-in-china-20230302-p5coyz. Accessed on 14.03.2023.

European Commission (2023a). Global Gateway. Retrieved from https://commission.europa.eu/strategy-and-policy/priorities-2019-2024/stronger-europe-world/global-gateway_en. Accessed 10.03.2023.

European Commission (2023b). EU-China agreement explained. Retrieved from https://policy.trade.ec.europa.eu/eu-trade-relationships-country-and-region/countries-and-regions/china/eu-china-agreement/agreement-explained_en. Accessed on 14.03.2023.

Harper, Jo (2022). Will the EU move to curb Chinese investments? Retrieved from https://www.dw.com/en/china-fears-eu-foreign-investment-strategy-at-a-crossroads/a-63546979. Accessed on 01.03.2023.

Huld, Arensde (2023). Prospects for European Companies in China in 2023. Retrieved from https://www.china-briefing.com/news/european-investment-in-china-prospects-for-2023/. Accessed on 07.03.2023.

Hutt, David (2023). European investors give China the cold shoulder. Retrieved from https://www.dw.com/en/european-investors-give-china-the-cold-shoulder/a-64270954. Accessed on 04.03.2023.

International Trade Centre (2023). Trade map. Trade statistics for international business development. Retrieved from https://www.trademap.org/Index.aspx?nvpm=1%7c%7c%7c%7c%7c%7c%7c%7c%7c%7c%7c%7c%7c%7c%7c%7c%7c. Accessed: 07.03.2023.

Lehne, Stefan (2022). Making EU Foreign Policy Fit for a Geopolitical World. Retrieved from https://carnegieeurope.eu/2022/04/14/making-eu-foreign-policy-fit-for-geopolitical-world-pub-86886. Accessed 14.04.2022.

McElwee, Lily (2023). Despite Beijing’s Charm Offensive, the EU-China Investment Agreement is Not Coming Back. Retrieved from https://www.csis.org/analysis/despite-beijings-charm-offensive-eu-china-investment-agreement-not-coming-back. Accessed 01.03.2023.

Mercator Institute for China Studies (2022). Chinese FDI in Europe: 2021 Update. Retrieved from https://merics.org/en/report/chinese-fdi-europe-2021-update. Accessed on 01.03.2023.

Stec, Grzegorz (2023). China’s EU policy and the art of strategic stalling. Retrieved from https://www.politico.eu/article/china-eu-policy-strategic-stalling/. Accessed on 10.03.2023.

Note: The views expressed in this blog are the author’s own and do not necessarily reflect the Institute’s editorial policy.